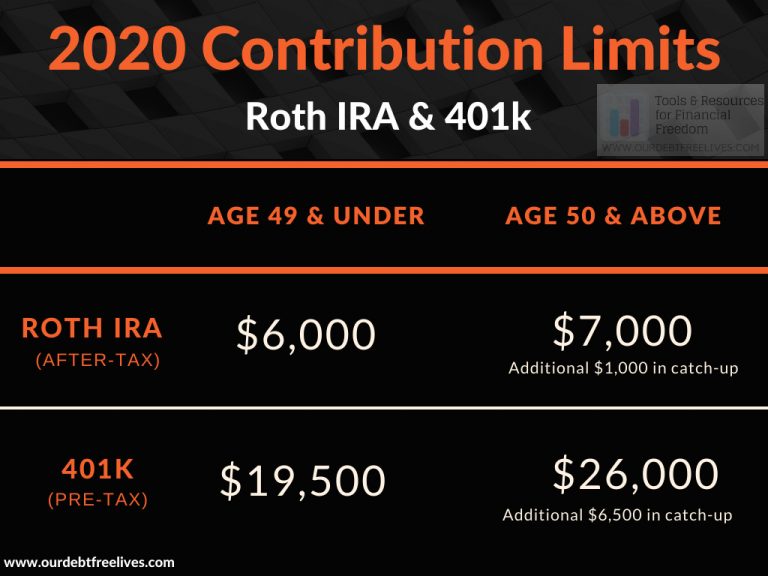

Roth IRA Contribution Limits 2025 are now in focus, impacting retirement savers across the nation. Understanding these changes is crucial for maximizing retirement contributions and minimizing potential tax liabilities. This year’s adjustments to contribution limits and income thresholds present both opportunities and challenges for individuals planning for their financial future. We’ll delve into the specifics of these changes, exploring the implications for various income levels and offering strategies for maximizing contributions.

The Internal Revenue Service (IRS) has announced the updated contribution limits for Roth IRAs in 2025, reflecting adjustments for inflation. These limits directly affect how much individuals can contribute to their retirement savings accounts, with separate limits for those under 50 and those age 50 and older. Further complicating matters are income limitations, which can restrict or even eliminate eligibility for Roth IRA contributions for higher earners.

This article will clarify these limits, providing a clear picture of who qualifies and how much they can contribute.

Roth IRA Contribution Limits 2025

Source: ourdebtfreelives.com

The year 2025 brings adjustments to Roth IRA contribution limits, impacting how much individuals can contribute towards their retirement savings. Understanding these changes is crucial for maximizing retirement planning and taking advantage of tax-advantaged growth. This article details the updated contribution limits, income restrictions, and strategies for optimizing Roth IRA contributions in 2025.

2025 Roth IRA Contribution Limits, Roth Ira Contribution Limits 2025

The maximum contribution amount for Roth IRAs in 2025 reflects an increase from previous years, offering individuals a greater opportunity to save for retirement on a tax-advantaged basis. These limits are adjusted annually to account for inflation and economic changes.

For individuals under age 50, the maximum contribution limit for 2025 is $7,

000. Individuals age 50 and older can contribute an additional $1,500, bringing their total maximum contribution to $8,

500. This reflects an increase from the 2024 limits. A comparison of the contribution limits across 2023, 2024, and 2025 is provided below:

| Year | Individual Limit (Under 50) | Individual Limit (50+) | Percentage Change from Previous Year |

|---|---|---|---|

| 2023 | $6,500 | $7,500 | – |

| 2024 | $6,500 | $7,500 | 0% |

| 2025 | $7,000 | $8,500 | 7.7% |

Income Limits for Roth IRA Contributions in 2025

Eligibility for full or partial Roth IRA contributions is subject to income limitations. These limits are based on your Modified Adjusted Gross Income (MAGI) and vary depending on your filing status. Exceeding these thresholds may reduce or eliminate your ability to contribute to a Roth IRA.

For single filers in 2025, the income limits for full Roth IRA contributions are estimated. For married couples filing jointly, the income limits are also subject to change based on IRS adjustments. The exact figures will be confirmed by the IRS closer to the tax year. The following illustrates potential scenarios:

Flowchart illustrating contribution scenarios (Illustrative, exact figures pending official IRS release):

The 2025 Roth IRA contribution limits are expected to be announced soon, impacting retirement savings strategies for many. For those seeking to bolster their income to maximize contributions, exploring additional employment options might be necessary; a quick search on sites like craigslist ukiah jobs could reveal opportunities. Ultimately, understanding these contribution limits is crucial for effective retirement planning.

The flowchart would visually represent the decision-making process based on MAGI. It would start with a question: “What is your MAGI?”. Based on the answer, the flowchart would branch into different paths, showing whether the individual can make a full contribution, a partial contribution, or no contribution at all. Separate branches would exist for single filers and married couples filing jointly, reflecting the different MAGI thresholds for each.

Impact of Spousal IRA Contributions

The income of one spouse can significantly impact the other spouse’s ability to contribute to a Roth IRA. Even if one spouse earns below the income limits, the higher-earning spouse’s income could affect both spouses’ eligibility for full contributions.

- Scenario 1: High-income spouse (MAGI exceeding limits) and low-income spouse (MAGI below limits). The low-income spouse may still be able to make a full Roth IRA contribution, depending on the specific income levels and the rules in effect for 2025.

- Scenario 2: Both spouses have high incomes (MAGI exceeding limits). Neither spouse may be able to make a full Roth IRA contribution. They may be eligible for a reduced contribution or none at all.

- Scenario 3: Both spouses have low incomes (MAGI below limits). Both spouses can likely make full Roth IRA contributions.

Strategies for Maximizing Roth IRA Contributions

Source: ourdebtfreelives.com

For those facing income limitations, several strategies can help maximize Roth IRA contributions. One popular approach is the “backdoor” Roth IRA contribution.

Backdoor Roth IRA Contributions: This strategy involves contributing to a non-deductible traditional IRA and then converting it to a Roth IRA. While this avoids income limitations on direct Roth IRA contributions, it can have tax implications and may not be suitable for everyone. Careful consideration of the tax implications is essential before employing this method.

Tax Savings Comparison (Illustrative Example):

| Income Level | Roth IRA Tax Savings (Illustrative) | Traditional IRA Tax Deduction (Illustrative) | Net Difference (Illustrative) |

|---|---|---|---|

| $50,000 | $700 | $1,000 | -$300 |

| $100,000 | $1,400 | $1,000 | $400 |

Note: The figures in this table are illustrative examples only and do not reflect actual tax savings, which are dependent on individual circumstances and tax brackets.

Potential Tax Implications and Considerations

Understanding the tax implications of Roth IRA withdrawals is crucial for effective retirement planning. Withdrawing contributions before age 59 1/2 is generally tax-free and penalty-free. However, withdrawing earnings before age 59 1/2 may be subject to both income tax and a 10% early withdrawal penalty, unless specific exceptions apply.

After age 59 1/2, withdrawals of both contributions and earnings are generally tax-free. However, certain circumstances may affect the tax treatment of withdrawals. Careful consideration of these implications is essential.

- Tax bracket at the time of contribution and withdrawal.

- Expected investment growth over time.

- Current and projected income levels.

- Other retirement savings options available.

Visual Representation of Contribution Limits

A line graph could effectively represent the relationship between income limits and contribution limits for Roth IRAs in

2025. The x-axis would represent Modified Adjusted Gross Income (MAGI), and the y-axis would represent the maximum Roth IRA contribution amount. Two separate lines would be plotted: one for single filers and one for married couples filing jointly. Each line would show how the maximum contribution amount changes as MAGI increases, eventually reaching a point where the contribution limit is zero for income above a certain threshold.

The graph would clearly illustrate the income thresholds at which full, partial, and zero contributions are allowed for each filing status. Different colors could be used to distinguish between single filers and married couples filing jointly. A clear legend would explain the meaning of each line.

Epilogue

Navigating the complexities of Roth IRA contribution limits in 2025 requires careful consideration of income thresholds and individual circumstances. While higher contribution limits offer increased retirement savings potential, income restrictions may necessitate strategic planning, such as exploring backdoor Roth IRA strategies. Ultimately, understanding these nuances empowers individuals to make informed decisions, optimizing their retirement savings and minimizing potential tax consequences.

Consult a financial advisor for personalized guidance tailored to your specific financial situation.